Latest Blogs

See More

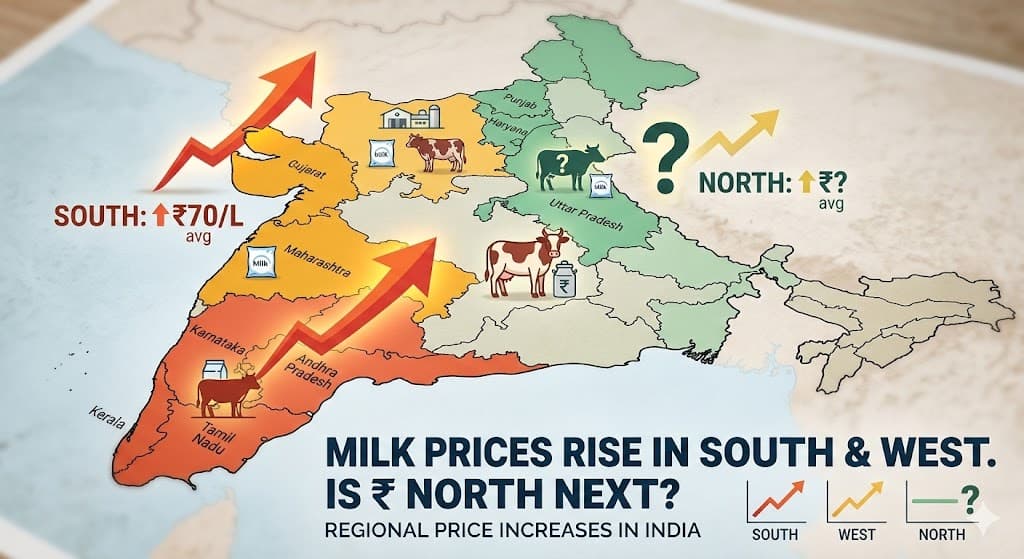

The recent round of retail milk price increases across South India and Maharashtra is no longer an episodic adjustment but a clear signal of structural stress building up in India’s milk economy. Over the past few months, multiple dairy companies in the southern states have revised retail prices upward by ₹2–₹3 per litre, largely through internal circulars rather than headline announcements. In Goa, the state cooperative Goa Dairy increased the price of full cream milk by ₹3 per litre, taking it from ₹67 to ₹70 per litre with effect from early December 2025. Similar ₹2 per litre increases have been implemented by several private and regional dairies across Karnataka, Tamil Nadu, Andhra Pradesh and Kerala, reflecting persistent supply tightness rather than temporary cost correction. Industry tracking platforms and sector-focused media have consistently flagged these increases, pointing to a region-wide pattern rather than isolated decisions by individual dairies.

This pressure on prices is directly linked to declining milk availability in the South, driven by prolonged heat stress, water scarcity and lower animal productivity. Several districts across southern states have reported milk yield drops in the range of 10–15 percent year-on-year, even as urban demand has remained steady. Compounding this is the steady rise in input costs — cattle feed, fodder, energy, packaging material and logistics — which has forced dairies to first increase procurement prices paid to farmers. Once procurement costs rise and remain elevated for multiple months, maintaining old retail prices becomes economically untenable. This reality has been openly acknowledged by major southern players such as Heritage Foods, whose management has publicly indicated that dairy prices, including liquid milk, would need to be raised by ₹1–₹2 per litre to offset rising operational costs.

A similar narrative has now unfolded in Maharashtra, where retail price increases have moved from proposal to implementation. In late February 2026, Gokul Dairy raised the retail price of buffalo milk by ₹2 per litre, from ₹74 to ₹76, explicitly citing fodder shortages, climate stress and higher procurement costs as the key reasons. This increase follows earlier revisions in 2025 and indicates that cooperatives in western India are facing sustained margin pressure. In parallel, retail milk associations in urban centres such as Pune have implemented ₹2 per litre hikes effective from March 1, 2026, reinforcing the view that Maharashtra is now firmly within the broader national milk inflation cycle.

Taken together, these developments point to three fundamental drivers behind the current wave of price increases. First is a genuine supply constraint caused by climate-linked production stress, particularly acute in southern states. Second is the sharp escalation in input costs across the dairy value chain, which has already been absorbed at the farmer procurement level and is now being passed on to consumers. Third is fodder scarcity, especially in states like Maharashtra, where erratic rainfall and seasonal disruptions have impacted livestock nutrition and productivity. These are not short-term aberrations but systemic issues that are reshaping milk economics.

Against this backdrop, the key question is whether North India will remain insulated. Historically, northern milk belts have benefited from stronger seasonal supply and relatively stable production, but even these regions are showing early signs of stress. Cooperatives such as Verka have, in the past, struggled to balance rising urban demand with procurement realities. Moreover, national-level price actions by Amul, which implemented a ₹2 per litre hike across markets in 2025, demonstrate that no region is entirely immune to cost-push inflation. If fodder prices remain elevated through summer or if climate volatility impacts yields earlier than expected, northern dairies will have limited headroom to absorb further cost increases.

In essence, the ₹2–₹3 per litre retail price hikes seen across South India and Maharashtra are not isolated price corrections but early markers of a deeper realignment underway in the dairy sector. Rising production costs, climate vulnerability, supply constraints and the imperative to sustain farmer incomes are converging to push milk prices upward. While northern markets have not yet seen the same intensity of revisions, the probability of spillover over the next three to six months remains moderate to high. Unless productivity improves or targeted policy interventions ease cost pressures, milk price inflation is likely to remain a defining feature of India’s dairy landscape through the rest of 2026.

Source : Blog by Kuldeep Sharma Chief editor Dairynews7x7.com

#MilkPrices #IndianDairy #DairyEconomics #MilkSupplyCrisis #FarmerFirst #FoodInflation