Latest Blogs

See More

Indian Dairy News

DairyNews7x7

Global Dairy News

DairyNews7x7

Source: Trade Data Monitor LLC

The other major driver of this change is the Chinese economy and its influence on demand, particularly for dairy in foodservice and elsewhere. The economy has not recovered in the way many had hoped post-COVID, with a pessimistic outlook for 2024, which reduces demand as consumers tighten their purse strings. This is seen especially in foodservice, where dairy is often incorporated in treaty dishes such as pizza or baked goods.

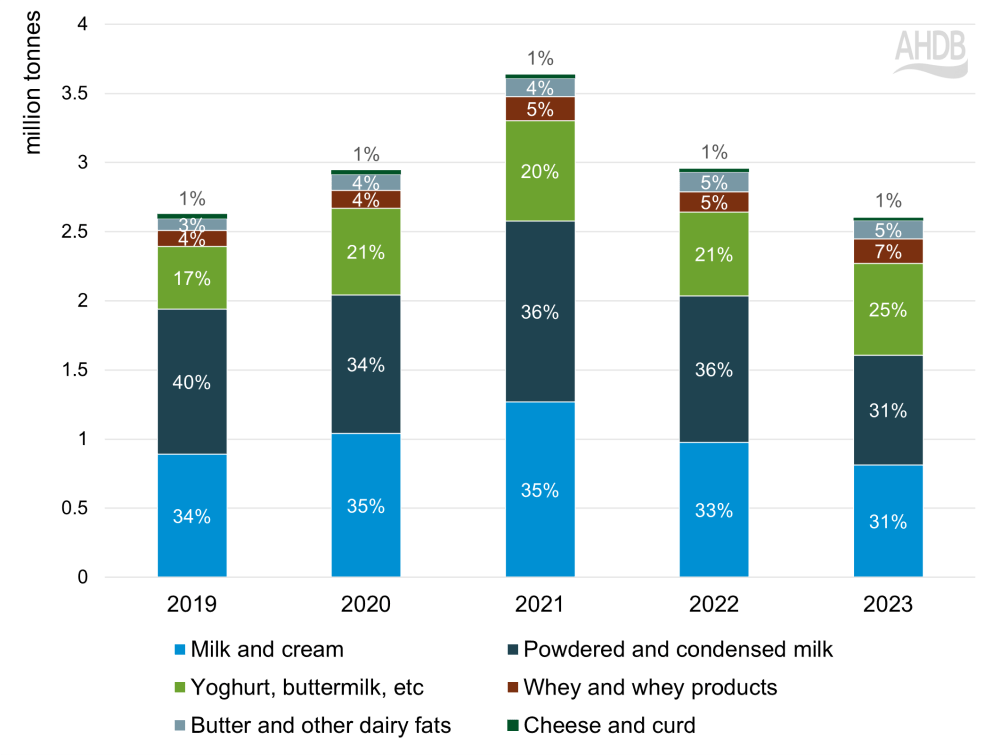

As domestic milk production increases, the need to import liquid milk and powders reduces. This is a trend we are already seeing come into effect through 2023 and expect to continue into 2024 and beyond. As milk and powders make up a substantial proportion of the Chinese import portfolio, these reductions are likely to have knock-on effects on global dairy trade, reducing demand, which may in turn soften prices.

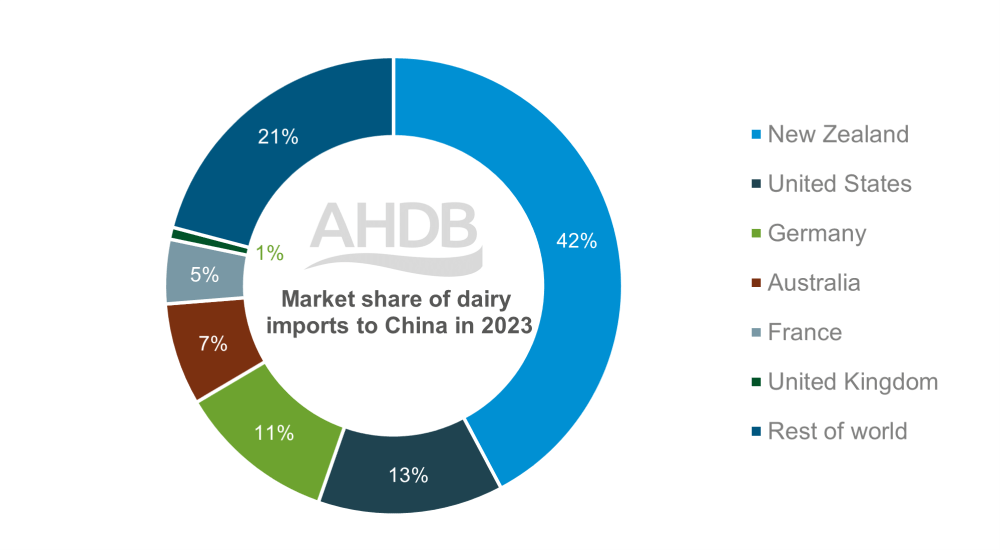

Looking at products in these key importers, 90% of US product imported in 2023 was whey or whey products. Meanwhile, UK imports to China were made of 72% milk and cream in 2023, equating to 16,000 tonnes.

Exports to China accounted for only 0.6% of total dairy exports from the UK in 2023, with a volume of 7,300 tonnes. Although export volumes are low, the influence of China’s trading and demand on the global market and dairy prices are important factors in our UK market.

Source: Trade Data Monitor LLC

Import volumes declined for all key regions into China, with New Zealand imports down nearly 183,000 tonnes in 2023 from the previous year. This may create a shift in global trading patterns, with New Zealand looking for alternative markets for products or diversifying production – for example, into cheese.

On the other hand, China’s domestic production of high-value products, such as butter and cheese, is limited by processing capacity, meaning there is potential for import demand growth in this area. This is hinged on the economic conditions in China, with heightened demand for butter in particular, for use in bakeries and foodservice, usually seen in times of economic growth.

Chinese cheese consumption has increased over the last few years, with a 16% compound annual growth rate between 2012 and 2022. In volume terms, Rabobank predicts that China’s cheese import demand will reach between 270,000 and 320,000 tonnes by 2030. This presents an opportunity for UK exports, particularly if catering to Chinese tastes in milder, creamy cheeses and cheese snacks.