Now that milk is flowing (in some countries well above the 3- and 5-year averages), commodity production appears to be running strong. Even in the lower production months ahead, that can have a big impact. Last week Germany’s numbers showed a 2.6% increase in milk collections, but almost 10% more butter production and 25% more SMP production. If these numbers continue at this pace, we expect EU commodity production data to hit an all-time high by the end of 2025.

Weather still poses a slowdown risk, of course. Partners in the UK and Ireland are reporting dry weather that might lead to lower milk collections, while the south of Europe is fighting fires and extreme heat. The question is how those weather extremes compare to last year and what that means for milk comparables.

Return of activity

Last week we debated with both the sales and purchase sides of the market whether demand for this year would return. Those active on the purchase side focused mainly on Q1 and even Q2/Q3 2026 demand. The majority seems covered for Q4. Last year, many buyers came back from their summer break still needing to cover the Christmas/Holiday/December demand. Asking around why the focus is different this year, answers varied.

Some are experiencing slower or hesitant demand and have pushed stocks into Q4, effectively covering part of the demand with unused stock. Some are still waiting for additional requests from their buyers in retail. It seems nobody wants to buy too much at these relatively high prices. But the majority cited last year’s rally as a reason to cover needs before going on break, fearful of a repetition of a price surge like last year.

On the sales side, we see a mirrored logic. Last year’s rally came as a surprise to many producers. The majority returned from their summer break oversold. With reduced milk production in the second half of 2024 still in mind as a likely scenario for this year, they seemed to have gone on holiday with fewer sales in their books. In addition, their logic is that—similar to last year—buyers will come back after their break, looking for their Q4 needs.

So the big market question is: who will turn up with bigger numbers—buyers or sellers? Judging from one week of activity, sellers appear ready for an end-of-year rally, while buyers show little interest in engaging yet. For powders—especially SMP—there is plenty of fresh product on offer from producers around €2,300 or slightly higher. Cheese producers are already showing some aged stock, with Irish cheddar coming close to €4,200, Gouda dropping below €4,000 (ages between 5–7 weeks), and mozzarella sellers eager to close some Q4 and Q1 sales.

And on our favourite product, butter… it seems some forgotten warehouses have been opened. With plenty of product from Q1 production this year (and even Q4 last year), producers are actively looking for quick offtakes. We see plenty of offers from French, Swedish, Danish and Polish products around. One of the bigger German producers reportedly offered sizable quantities to almost all traders, signalling that supply is unlikely to be an issue this year. Only the Irish still manage the hide-and-seek game best. With strong export numbers continuing to surprise, they show no pressure to sell for now. But with sufficient stocks from Sweden, France, Germany, Poland and Denmark, it’s only the buyers who specifically need Irish product that might have to pay up; those with options have plenty of alternatives.

One thing seems sure: whether buyers or sellers lead the way back this week, activity and volatility will be joining the party.

Butter: Bounce or Break?

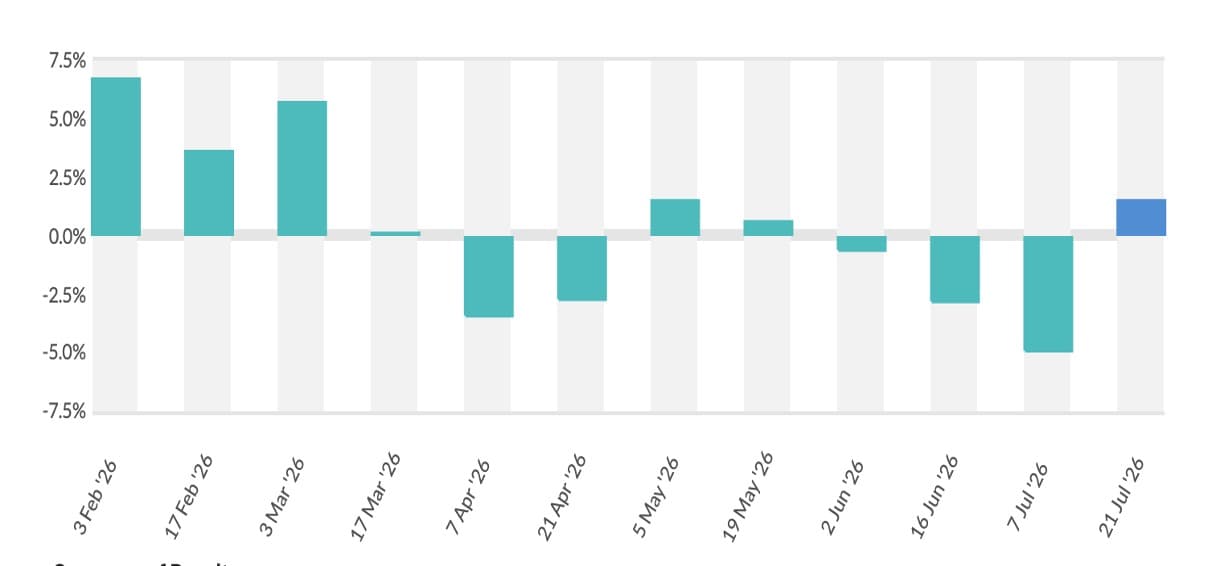

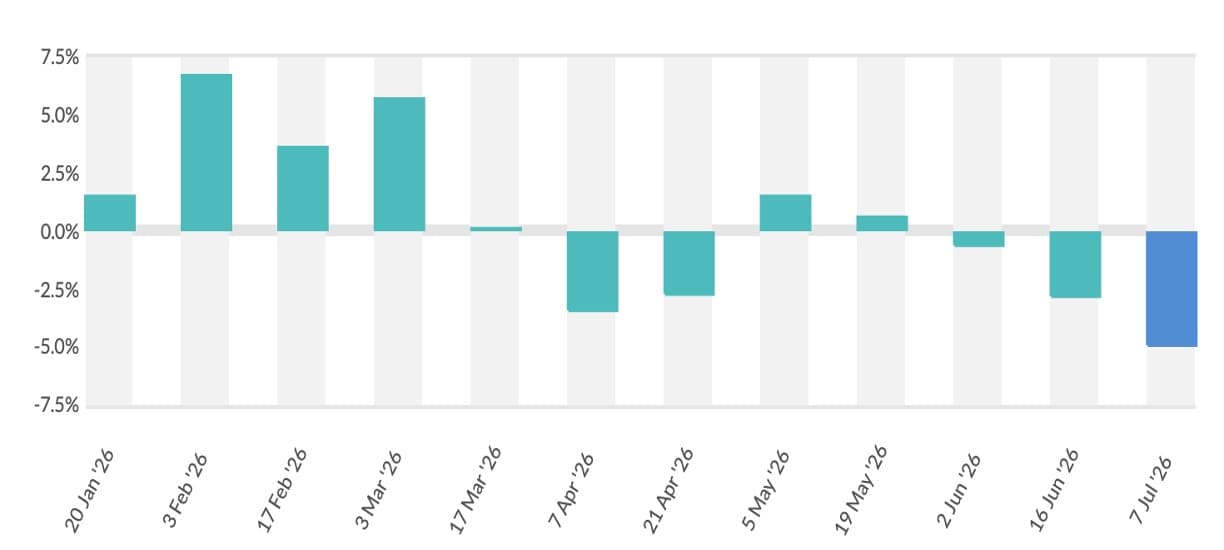

Butter took a clear step down last week. Trading at € 6685 for Q4 and € 6600 for Q1 on NL/DE/BE butter, the market is about € 150 lower than the week before. Looking back to 2022, the market held above € 7000 until mid-September, it was only than that cream prices broke and Q4 demand proved too weak to support the market. A similar move could occur this year, keeping the markett afloat for a few more weeks. On the other hand, last year, the last week of August pushed cream to € 10,000 before easing back during September; if that repeats, prices could start to slide again once cream loses firmness. Some spot offers for cream around € 8000 last week point to the latter scenario.

Our expectation is that if producers who actively sought buying interest at the end of last week don’t see indications that demand will return, we’re set up for a 2022-style sell-off, taking prices back to—and possibly below € 6000. We know this forecast may draw criticism, but a 10% decline in butter versus other agro commodities would still feel like a modest correction to us. If production numbers continue to rise as the trend suggests, producers may have to brace for a deeper drop. Keep in mind that in 2022, butter fell from € 7200+ in August to € 4300 in February.

For those comparing data: butter and AMF imports in 2022 YTD (June) totaled 11.500 mt, with 2025 imports already at 25.000 mt. Exports that year dropped >5.5% to 105.000 mt YTD in June, exactly the same as last year. Butter production this year is up roughly 10% (≈10.000 mt) versus 2022. So, saying the years are not comparable… we can find some similarities.

That said, we start the week with the following offers:

- 6 loads of Irish butter for September at € 6700 FCA Ireland

- 6 loads of Polish Sweet Cream for September at € 6800

- 4 loads of Polish lactic for August/September at € 6750

- 9 loads of NL/DE/BE butter for Q4 at € 6700

- 12 loads of Irish butter for December / January at € 6500 (winter product)

- 12 loads of Irish butter for Q1 at € 6550

- 12 loads of NL/DE/DE butter for Q1 at € 6625

- 12 loads of Polish lactic for Q1 at € 6550

Bids seen last Friday (sentiment weak; several buyers pulled out):

- 12 loads of Irish butter for Q1 at € 6450

- 12 loads of Irish butter for Q1 at € 6400

- 9 loads of NL/DE/BE butter for Q4 at € 6550

- 6 loads of Irish lactic (good FFA) for December at € 6425

Cheese: On the break as well

Keeping it short, as most of what we want to say for cheese we have already said for butter. Sellers are waiting for the return of buyers, but speaking to industrial buyers, sellers might be waiting up until Christmas. Demand seems largely covered and is unlikely to match increased production. Demand for WPCs and other high whey-protein products is keeping a bit of margin for producers, but we fear that won’t last. Although official quotations are still much higher, we keep hearing that lower prices are being booked out of sight of the market.

Gouda prices between € 3800–€ 3900 for Q4 and Q1 are possible when buyers take volume. Cheddar in the UK and Ireland—some even claim purchases below € 4200. On mozzarella, we hear a wide range: as low as € 3750 Q4 from one buyer and as high as € 4000 from a producer for last-minute sales.

But the data show a bearish scenario. EU cheese production is at its highest level in at least five years. At the same time, imports have risen versus last year, while exports YTD (June) show the EU isn’t taking any extra volumes. With our forecast that butter prices are likely to lose 10–15% over the next few months, cheese seems very likely to follow. We would expect Gouda/Edam/Mozzarella prices over the next week to drop toward € 3500–€ 3600.

We start with sellers