Latest Blogs

See More

Indian Dairy News

DairyNews7x7

Global Dairy News

DairyNews7x7

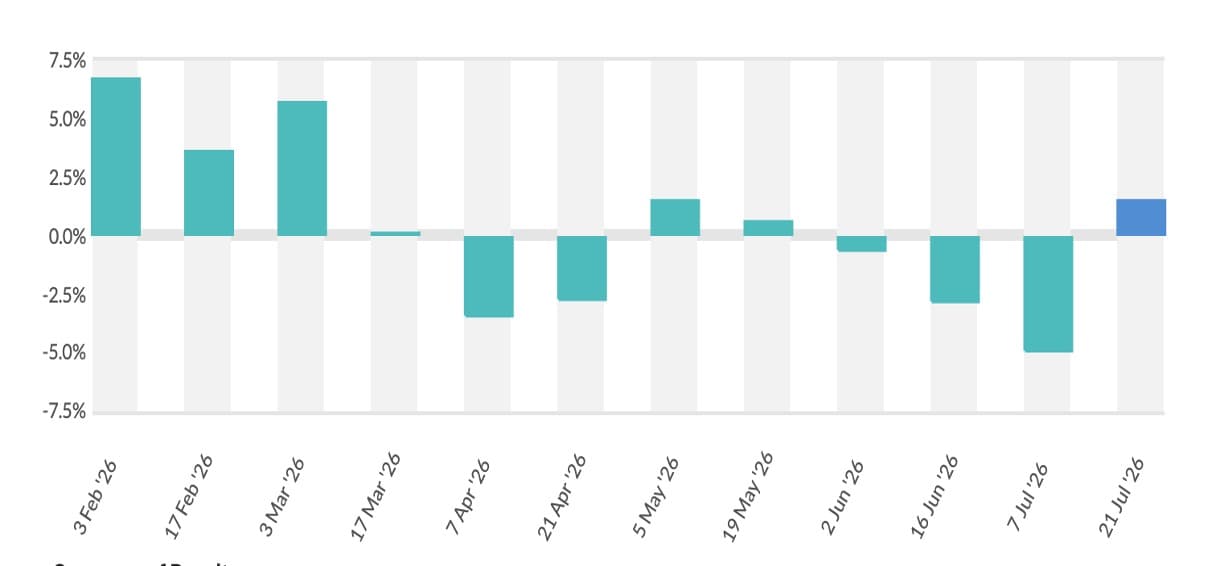

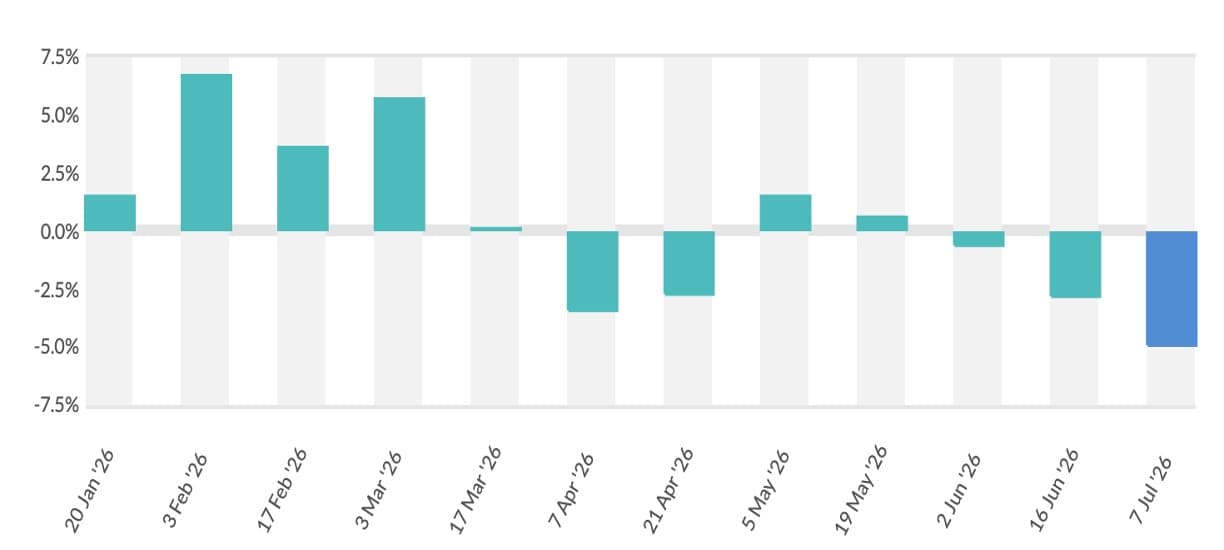

The outcome of Global Dairy Trade Event 394 held on 16 December 2025 confirms a decisive bearish turn in the global dairy commodity cycle, with the GDT Price Index falling sharply by 4.4% to an average price of USD 3,341 per tonne (€2,843). The correction was led by dairy fats and powders, underscoring weak buyer appetite amid comfortable global supply. Whole Milk Powder (WMP) recorded a steep 5.7% decline, while Skim Milk Powder (SMP) prices eased by 2.1% to USD 2,431 per tonne (€2,068), reaffirming sustained pressure in bulk ingredients driven by subdued demand from key Asian markets. In the fat segment, Anhydrous Milk Fat (AMF) fell 5.2% to USD 5,602 per tonne (€4,766), while butter declined by 2.5% to USD 5,012 per tonne (€4,264), indicating that the earlier correction in fats is continuing rather than stabilising.

In contrast, selective strength in value-added products provided some counterbalance to the broader decline. Cheddar prices remained unchanged at USD 4,646 per tonne (€3,953), reflecting stable demand fundamentals, while Mozzarella rose sharply by 6.7% to USD 3,395 per tonne (€2,888), signalling resilience from foodservice-linked consumption. The standout performer was lactose, which surged 14.4% to USD 1,430 per tonne (€1,217), pointing to tightening availability and niche demand strength. Overall, Event 394 highlights a clear divergence within the dairy complex, where bulk commodities continue to weaken while functional and application-driven products show relative resilience. For trade participants, the results reinforce expectations of continued volatility and limited near-term upside, with market recovery likely to be uneven and product-specific rather than broad-based.

The immediate context is set by Event 393, where the GDT Price Index declined sharply by 4.3%, reinforcing a bearish undertone that has been building since mid-2025. The weighted average price across all commodities traded at Event 393 stood at approximately USD 3,507 per tonne, reflecting a broad-based correction across key product categories.

Powder markets, which remain central to global dairy trade flows, continued to soften, with Whole Milk Powder (WMP) prices declining by around 2.4% to USD 3,364 per tonne, while Skim Milk Powder (SMP) eased by about 1.6% to USD 2,498 per tonne. The sharper pressure was visible in the dairy fat segment, where butter prices fell by nearly 12.4% to around USD 5,169 per tonne, and anhydrous milk fat (AMF) declined by approximately 9.8% to USD 5,902 per tonne. The only notable exception in the product basket was cheddar cheese, which registered a price increase of about 7.2% to USD 4,639 per tonne, highlighting selective demand resilience in value-added categories even as the broader market weakened. Total traded volumes at Event 393 were around 34,282 metric tonnes, indicating that participation levels remain healthy, though buyer behaviour is increasingly price-conscious.

This outcome at Event 393 aligns closely with the broader pattern observed across several GDT auctions in the second half of 2025, a trend extensively covered in recent DairyNews7x7 fortnightly analyses. After a relatively firm first half of the year, supported by supply tightness and firm demand, global dairy markets entered a correction phase as milk production in major exporting regions — including Oceania, the European Union and North America — showed resilience and inventories gradually rebuilt. This improved supply situation, combined with cautious buying from key import regions, has shifted negotiating power towards buyers, particularly for powders and dairy fats.

Demand signals remain mixed. While there is no evidence yet of a strong rebound from major Asian importers, particularly China, certain segments such as cheese continue to benefit from steady foodservice and retail demand in Western markets. Futures and derivatives linked to GDT settlement prices suggest that both producers and traders are hedging cautiously, reflecting expectations of continued volatility rather than a sharp rebound in the near term. The prevailing sentiment going into Event 394, therefore, is one of consolidation, with downside risks still outweighing immediate upside catalysts.

Looking ahead into early 2026, powder markets are expected to remain largely range-bound to slightly soft in the absence of a material demand resurgence from Asia. Seasonal demand may provide some support toward late Q1 or early Q2, but any sustained recovery will likely depend on renewed buying interest from China and Southeast Asia. Dairy fats could continue to face pressure in the short term due to ample availability, although rising cream costs and steady retail demand may limit the extent of further declines. Cheese and other value-added categories are expected to outperform bulk commodities, benefiting from more stable consumption patterns and better price realisation.

For the Indian dairy sector, the implications of the recent GDT trajectory and the upcoming Event 394 are significant, even though domestic milk prices are not directly linked to global benchmarks. Softening global powder prices tend to influence export parity calculations for Indian processors, particularly for SMP and WMP shipments to markets in the Middle East, North Africa and parts of Southeast Asia. Periods of weakness at GDT auctions often create competitive windows for Indian exporters, provided logistics and regulatory clearances align. At the same time, subdued international prices can put pressure on domestic powder conversion economics, influencing procurement and inventory decisions by large processors.

From a strategic standpoint, Indian dairy companies and traders would benefit from closely tracking GDT signals for timing exports, managing inventories and structuring forward contracts. The recent divergence between bulk powders and value-added products also reinforces the case for Indian players to strengthen portfolios in cheese, fat-based ingredients and specialised dairy products, which tend to offer greater pricing resilience during global downturns. As Event 394 unfolds, it will serve as a crucial indicator of whether the global dairy market has found a floor or whether further adjustments lie ahead as the sector moves into 2026.

Source : Dairynews7x7 Dec 16th 2025 Global Dairy Trade Event 394