Latest Blogs

See More

Indian Dairy News

DairyNews7x7

Global Dairy News

DairyNews7x7

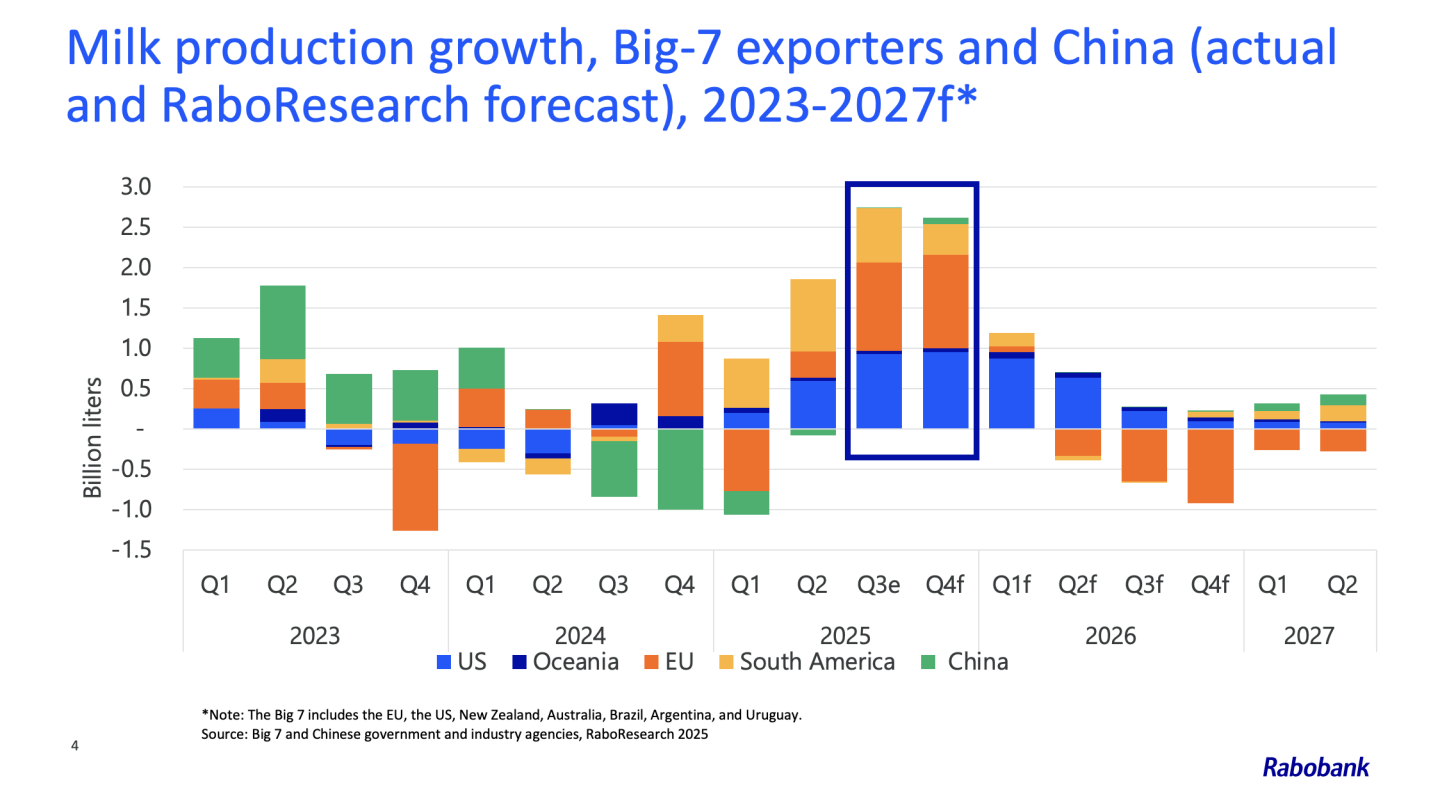

Global milk production across major dairy-exporting regions has surged in 2025. According to an analysis cited by DairyHerd, year-to-date (through July) output among the top export markets is up by about 1% compared to 2024, adding approximately 3.7 billion pounds of milk to global supply.

That surplus is big enough to produce hundreds of millions of pounds of additional dairy commodities — extra cheese, butter, milk powder etc.

But global demand — both domestic consumption and international trade — is not rising at the same pace. Export markets are showing signs of fatigue, and many regions are already reporting growing inventories and falling or volatile commodity prices.

As a result, the “glut” is pressuring prices across the board — butter, SMP/WMP, cheese, whey, etc — squeezing margins for both producers and processors.

In short, the global dairy market is facing a structural oversupply — what analysts are calling a “global milk glut” or “wall of milk” — which is raising serious concerns about sustainability of dairy incomes and price stability.

Even though this is a global phenomenon, it has important implications for India, because:

India is a major global producer, and Indian processors often compete (directly or indirectly) with global commodity markets for exports (e.g. SMP, WMP, butter, cheese, etc.).

If global commodity prices remain depressed due to oversupply, export-oriented dairy producers in India may find margins squeezed — especially in SMP, WMP, butter, cheese.

Domestically, while liquid milk consumption may remain stable (due to population & demand growth), value-added segments might suffer if export-driven demand slows, or if global oversupply depresses international reference prices (which often influence local wholesale rates).

For investors / entrepreneurs looking to build large-scale dairy processing plants (cheese, SMP/WMP etc.), the surplus means heightened market risk — oversupply could erode returns, especially if demand doesn’t pick up as expected.

At the same time:

For domestic-market–oriented dairy, this could mean lower raw-milk procurement costs (if global price pressure drags domestic prices down), which could benefit processors focusing on value-added products for the Indian market (cheese, paneer, ghee, etc.), assuming domestic demand holds.

But for farmer incomes — especially those relying on commodity exports or on cooperatives active in global supply chain — the “glut” may erode their profitability unless supply is managed or value-addition is promoted.

Given this global scenario, stakeholders — especially in India — would do well to:

Focus on domestic demand growth and value-addition, rather than relying heavily on commodity exports. Products like cheese, whey-based ingredients, specialized dairy foods (high-protein, fortified, functional dairy) for the domestic market may offer better resilience.

Diversify product mix: combining commodity (milk powder, butter) with value-added and niche products to reduce exposure to volatile global prices.

Push for supply moderation and milk production management (through seasonal strategies, smarter herd management, production planning) to avoid contributing to global oversupply at peak flush.

Strengthen supply-chain and cost control, to remain competitive even if global prices are depressed — including efficient processing, lower wastage, rational raw-milk procurement costs, and closer integration between production and demand.

Leverage policy support and domestic demand tailwinds (population growth, increasing per-capita consumption, rising demand for dairy proteins) to create stable long-term growth even if global export markets are shaky.