Latest Blogs

See More

Indian Dairy News

DairyNews7x7

Global Dairy News

DairyNews7x7

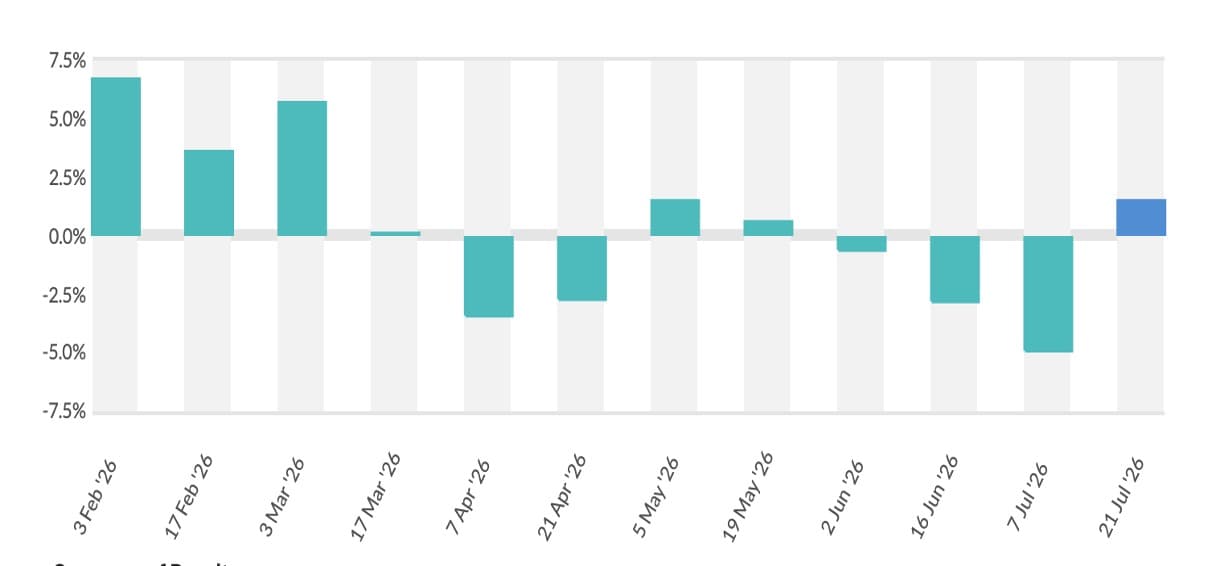

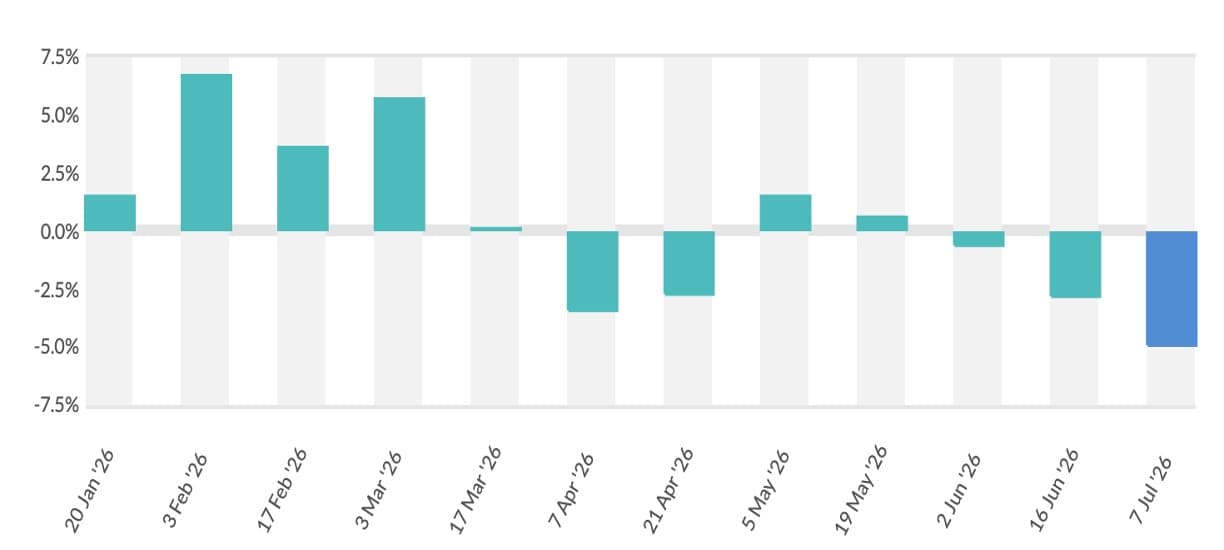

European raw-milk prices have plunged to their lowest in five years, as oversupply and weak demand weigh on dairy markets across the region. According to recent data from DCA Market Intelligence B.V., benchmark prices for unprocessed milk have slipped below € 25 per 100 kg, a level not seen since 2020.

The downturn is not confined to raw milk alone: prices for skimmed milk concentrate (SMC) have also dropped sharply, falling below €1,000 — a first since the onset of the COVID-19 pandemic. Cream, butter and other dairy-fat products are under pressure too, with butter prices hovering near €4,000 per metric tonne and cream prices tumbling despite the usual pre-Christmas seasonal lift.

Cheese markets in Europe are also feeling the strain. Mozzarella, for example, dropped nearly 5% week-on-week, while other varieties such as Emmental are witnessing wide price dispersion and downward pressure.

Market analysts attribute this slump to a persistent glut of raw milk — enabled by high production levels across north-western Europe — combined with weak demand domestically and internationally. Many processors are reportedly struggling to find buyers for both whole- and skimmed-milk deliveries.

Exporters face squeezed margins: With European milk-fat products and powders declining, countries and firms relying on exports of SMP/WMP, butter or cheese may see revenues fall. This will likely pressurize farm-gate milk prices, particularly in surplus-producing regions.

Incentive to shift toward value-added and domestic-market dairy: As bulk-commodity prices drop, dairy players — producers, cooperatives and processors — may pivot to value-added liquid milk, branded yogurt/cheese, and other retail-facing products less tied to global commodity cycles.

Global oversupply risk extends beyond Europe: Surging European output, when combined with oversupply trends elsewhere (New Zealand, US, certain developing nations), could depress global commodity-dairy prices for prolonged periods, forcing a re-evaluation of investment in volume-centric dairy export models.

Potential ripple effect on developing-country dairy sectors (e.g. India): Lower global dairy commodity prices may reduce export demand from Asia & Africa for SMP/WMP or butter, reducing export-led upside for large dairy producers. This could shift focus back to domestic demand, value-added products, and quality differentiation.

Whether European milk producers begin to cut production or dry off cattle to stem oversupply — reduction in output could help stabilize prices.

Movement in global demand for dairy powders, especially from traditional importers (Africa, Middle-east, S-East Asia) — if these markets pick up, prices may bounce back.

Policy measures or support packages for farmers (subsidies, production quotas, supply-management) — such interventions may shape the next 6–12 months for dairy prices.