While going through the agenda of this upcoming dairy event "International Dairy Processing Conference (IDPC) 2026" curated by TPCi, I found the choice of sessions extremely relevant and timely for the Indian dairy sector. This prompted me to curate a series of deep-dive articles around these themes, aimed at drawing practical insights for the benefit of the wider dairy industry.

With milk production crossing 247.87 million tonnes, India contributes nearly 24% of global milk output, engaging over 8 crore farmers, most of them smallholders. Yet, as the sector looks toward Vision 2047, the challenge is no longer scale alone. The real question is how India transitions from a volume-led dairy economy to one driven by value, sustainability, competitiveness, and farmer resilience—while remaining affordable and inclusive.

Vision 2047 places dairy at the heart of rural India.

Dairy continues to be the backbone of rural livelihoods, nutritional security, and women-led income generation. However, rising costs of

feed, fodder, energy, labour, and compliance, coupled with climate stress, are squeezing farm-level economics. The Vision 2047 roadmap therefore calls for a broader definition of self-reliance—one that integrates

productivity improvement, resource efficiency, climate resilience, and assured farmer remuneration, rather than mere production expansion.

Global dairy dynamics are rapidly reshaping benchmarks.

Internationally, dairy markets are witnessing slower volume growth but faster innovation. Developed economies are focusing on

functional dairy, low-carbon processing, digital traceability, and premium nutrition, while emerging markets drive demand for affordable proteins. India’s dairy exports—currently around

USD 500–600 million annually (inclusive of sweets, casein, lactose being cosidered in other categories)—remain modest relative to its production strength, highlighting both untapped opportunity and structural gaps in

quality alignment, product mix, and cost competitiveness.

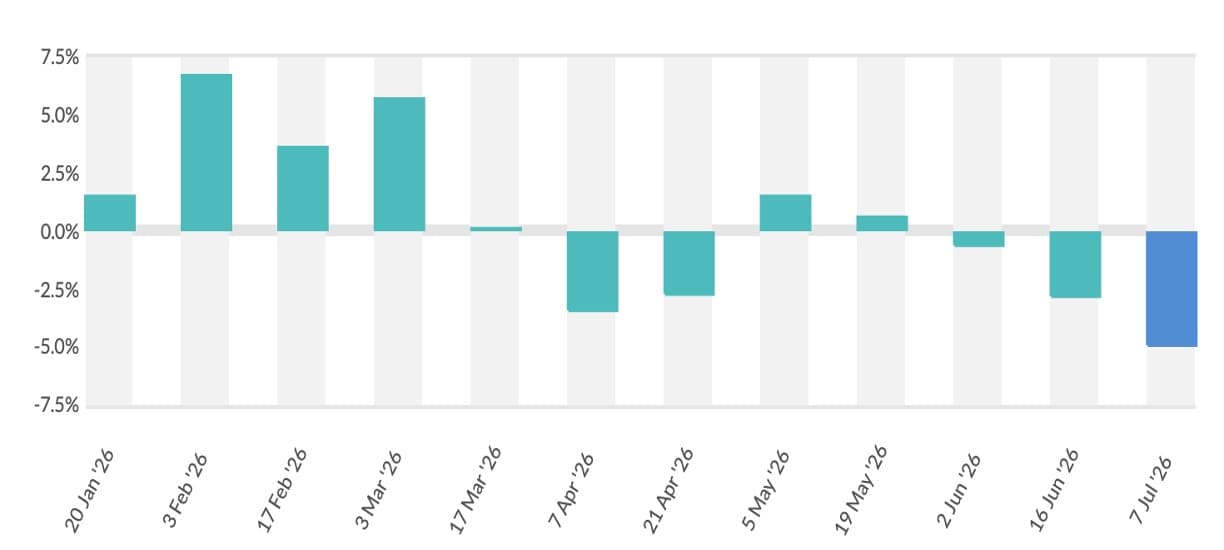

Current market conditions reflect both volatility and opportunity.

Domestic dairy demand continues to grow at

5–6% annually, supported by urbanisation, rising incomes, and evolving consumption habits. At the same time, processors face margin pressure due to volatile SMP and butter prices, higher packaging costs, logistics inflation, and working capital stress. This environment underlines the need for

market-linked procurement, sharper price risk management, and demand-driven production planning, especially for commodities like SMP.

Value addition remains India’s biggest unrealised lever.

Less than

30% of India’s milk is converted into value-added products, compared to

70–80% in mature dairy economies. This structural gap limits profitability and export readiness. Emerging segments such as

cheese, fermented dairy, high-protein products, lactose-free milk, fortified nutrition, whey derivatives, and ethnic dairy with global appeal offer pathways to improve margins while meeting evolving consumer expectations.

Processing innovation is moving from choice to necessity.

Advanced technologies—membrane filtration, enzymatic processing, shelf-life extension, clean-label formulations, and precision fermentation interfaces—are reshaping dairy processing globally. For Indian dairies, especially in emerging markets, innovation must balance

cost sensitivity with scalability, ensuring that technology adoption translates into commercial viability rather than only pilot success.

Cooperatives and private players remain twin pillars of growth.

India’s cooperative model continues to anchor farmer aggregation, price stability, and rural inclusion. Simultaneously, the private sector has driven

branding, efficiency, product diversification, and modern retail integration. Future sectoral growth depends less on competition and more on

complementarity—leveraging cooperative scale with private sector agility through partnerships, shared infrastructure, and technology-enabled procurement systems.

States are emerging as strategic dairy growth engines.

State-led initiatives in breed improvement, fodder development, chilling infrastructure, and processing capacity are reshaping regional dairy landscapes. States such as

Uttar Pradesh, Rajasthan, Gujarat, Maharashtra, Karnataka, and Telangana are increasingly aligning dairy growth with rural prosperity and employment. Coordinated state–centre strategies will be crucial to avoid fragmented capacity creation and uneven value realisation.

Technology is redefining the dairy value chain.

From

digital milk testing and AI-led herd management to smart factories and real-time quality monitoring, technology adoption is improving efficiency and reducing losses. Equally important is the rise of

waste valorisation, whey utilisation, energy recovery, and advanced effluent treatment, positioning dairies to move toward circular and climate-resilient operations—an emerging expectation rather than a future ambition.

Automation, packaging, and IQF are enabling scale with consistency.

Automation is addressing labour shortages while enhancing hygiene, traceability, and throughput. Modern packaging—aseptic, portion-controlled, and shelf-stable formats—along with

IQF technologies, is expanding product reach across geographies and channels. These capabilities are critical for both domestic distribution and export-oriented growth without compromising quality.

Quality certification and food safety are now market passports.

As India aspires to deepen its global dairy footprint,

quality assurance, testing integrity, and certification compliance are non-negotiable. Alignment with

Codex, FSSC, ISO, and residue standards, supported by robust testing infrastructure, will determine export credibility. Importantly, stronger quality systems also reinforce trust in domestic markets, where consumers are becoming increasingly discerning.

The road ahead demands a strategic reset.

The collective themes of this conference reflect an industry in transition—from commodity dependence to

value-led growth, from isolated interventions to

system-wide integration, and from short-term price management to

long-term farmer and processor viability. Achieving Vision 2047 will require balanced policies, responsible innovation, and market structures that reward efficiency without undermining the farmer at the foundation of the dairy ecosystem.

I sincerely invite industry colleagues, professionals, and young dairy leaders to register for this event through the link below and be part of these important conversations—because collective learning and shared wisdom will shape the future of Indian dairy.

Link for registration in IDPC 2026 conference on 7th Dec 2026 at Yashobhoomi Dwarka Delhi .

Source : Dairynews7x7 Dec 15th 2025, Blog by Kuldeep Sharma Chief Editor Dairynews7x7