Latest Blogs

See More

Indian Dairy News

DairyNews7x7

Global Dairy News

DairyNews7x7

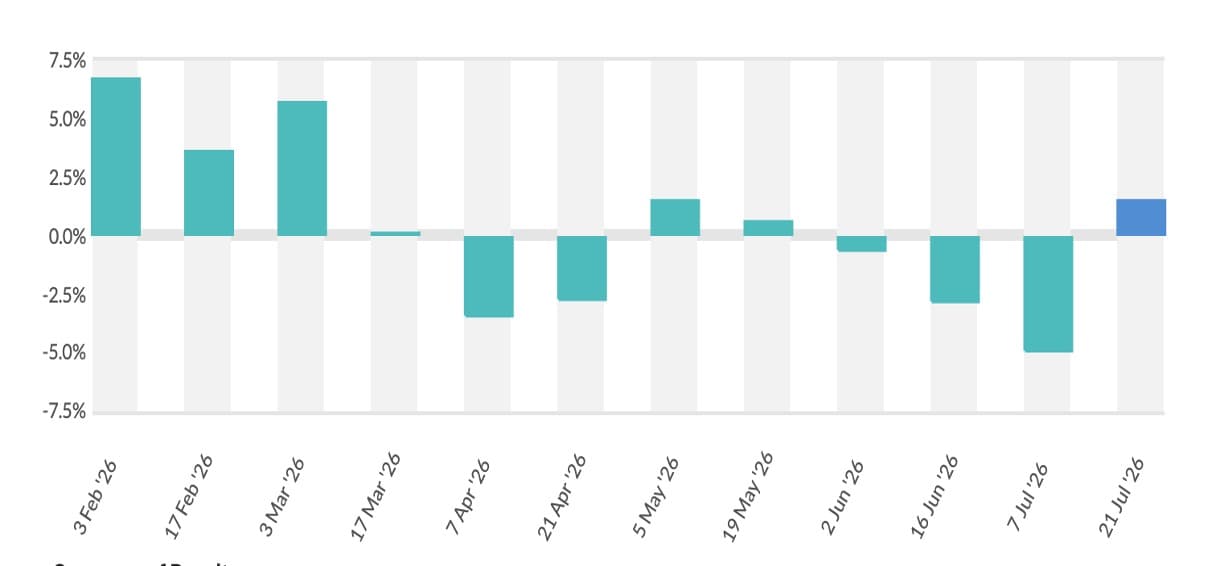

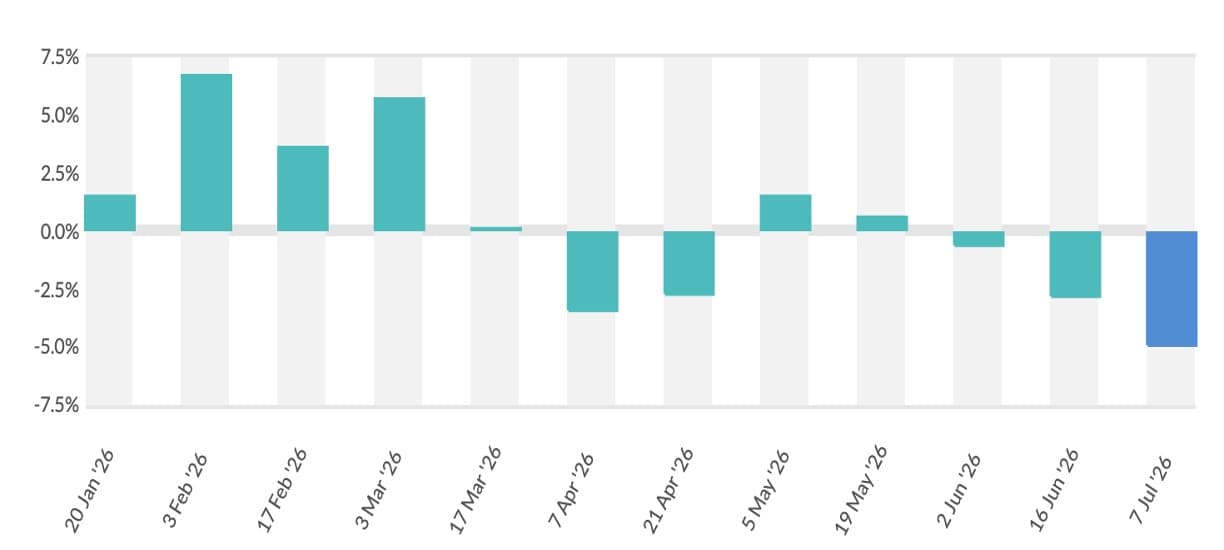

The 396th Global Dairy Trade (GDT) auction — the second dairy trading event of 2026 — delivered a second consecutive rise in global dairy prices, with the GDT Price Index increasing by 1.5 % to 1,088 compared with the January 6 event (which had climbed about 6.3 % to 1,072 after nine straight declines).

The latest auction saw 27,821 metric tonnes of dairy commodities sold, slightly below the ~29,282 t offered at the first event of the year, involving 164 registered bidders and 114 winning participants across 19 bidding rounds. Looking at individual product movements, anhydrous milk fat (AMF) prices rose sharply by approximately 3 % to about €6,191/mt, skim milk powder (SMP) increased about 2.2 % to ~$2,615/mt, butter gained around 2.1 % to roughly $5,314/mt, and whole milk powder (WMP) ticked up about 1 % to ~$3,449/mt. In contrast, some cheese categories softened, with mozzarella down about 2.3 % to ~$3,340/mt, cheddar down around 1.4 % to ~$4,594/mt, and lactose sliding ~1.8 % to ~$1,385/mt.

This latest uptick comes on the heels of the initial January bounce, which interrupted a prolonged nine-event downturn through late 2025, a period marked by surplus milk production and subdued buying interest that had pushed the index lower. The first rebound in early January reflected a partial balancing of supply with renewed demand and tighter offer volumes in some categories. The follow-up rise in Event 396 suggests that buyers continue to test firmer pricing levels for core dairy commodities, even as market sentiment remains cautious.

Drivers of the recent increases include modest improvements in export demand — particularly for fats and powders — amid signs of stabilising import interest from key regions, along with seasonal shifts in milk flows that sometimes tighten exportable availability after peak production months. However, the presence of weaker prices in select cheese and lactose lines highlights continuing divergence across product classes.

Near-term outlook: The back-to-back price rises signal that international dairy prices may be emerging from the downward cycle of late 2025, but sustainability depends on persistent demand and disciplined supply. Should import appetite remain firm — supported by global foodservice recovery and stock rebuilding — and if exporter volumes ease post-peak production, prices could consolidate or advance gradually. Conversely, continued high global milk output and inventory levels mean that prices may remain volatile and susceptible to renewed downward pressure, especially if buying interest falters.

Source : DAirynews7x7 Jan 20th 2026 GDT